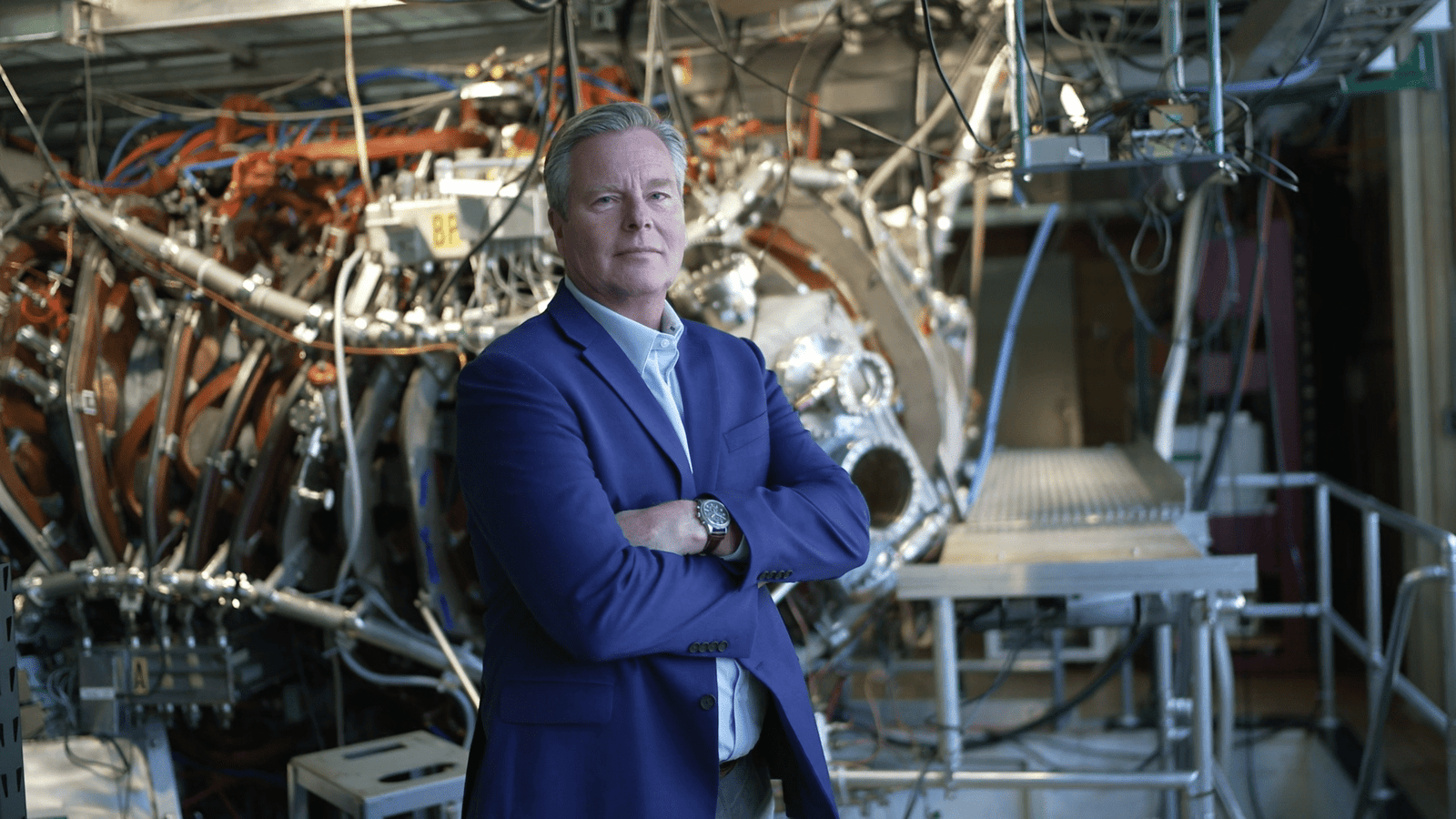

Fusion energy has been around for decades proving it can work. Chris Mowry, an energy industry veteran with more than 30 years of experience, focus on something more difficult: proving it can sell. As CEO of The first type of energya fusion startup backed by Bill Gates’ Breakthrough Energy Ventures, Mowry is pushing the industry beyond scientific milestones and into real-world power economics. His test is straightforward: Can fusion meet the same standards that apply to any energy source: reliability, cost and availability.

“The real transition to commercialization is signaled when end customers start paying companies for their fusion technology itself, rather than a contingent commitment to buy electricity if it is produced sometime in the future,” he told the Observer.

This change is becoming more urgent. Fusion attracted more than 10 billion dollars in funding in 2025, driven in part by increased electricity demand from AI data centers. But most service agreements across the sector still lack firm financial commitments.

Mowry’s perspective comes from decades inside the energy system the merger aims to disrupt. He started at Philadelphia Electric and the Institute of Nuclear Power Operations, then spent 10 years at GE Energy in senior roles. He later headed B&W Nuclear Energy, started a small modular reactor business and served as CEO of General Fusion. In these roles, his focus has been consistent: turning complex energy technologies into sustainable businesses. That operational discipline now shapes Type One.

Founded in 2019 by University of Wisconsin fusion scientists, including chief science officer John Canik, the company has raised more than $160 million. Mowry joined in 2023 after working with Advanced Energy Enterprises to improve its trading strategy.

While fusion remains a race between competing designs, Type One is betting on the stellarator, a reactor built for stable, continuous operation that’s closer to how utilities use baseload power today. Mowry argues that alignment with existing network needs is critical.

“The stellarator is the only fusion technology currently demonstrated to work stably and continuously,” he said.

The company’s strategy is already taking shape through a partnership with the Tennessee Valley Authority (TVA), the largest public electricity provider in the US. The two are developing what could become the first commercial star plant in TVA’s Bull Run area, a retired coal plant.

For Mowry, the partnership is just as important as the technology. TVA is not just a prospective customer; is helping shape licensing, development and deployment. This reflects Type One’s broader approach of integrating into the existing energy system rather than reinventing it.

Rather than building everything in-house, the company relies on established industrial partners for manufacturing and plant systems, while focusing on its core fusion technology. The goal is to reduce execution costs and risk.

“Our business plan is relatively capital efficient by design,” Mowry said.

Type One aims for initial operations in the early 2030s, with subsequent plants designed to scale up faster and cheaper. Mowry believes fusion could eventually follow a production model rather than the slow, custom build typical of large energy projects.

Type One is not alone in pursuing this vision. Commonwealth Fusion Systems, backed by investors including Googleis advancing a tokamak design with plans for deployment in the early 2030s. Helion energysupported by Sam Altmanis taking a different approach with a pulsed system and aims to give Microsoft 50 megawatts by 2028.

Each path reflects different technical and economic bets, and the outcome remains uncertain. But Mowry argues that the industry is entering a new phase. Once a company secures a dedicated customer—as Type One has with TVA—the conversation begins to change. The essential question is no longer physics, but execution.

“There simply isn’t enough early-stage capital around the table to fund even a modest number of more than $10 billion in technology development programs,” Mowry said. “Investors are increasingly asking the questions they raise with growth-stage companies. These are about business experience and deployment more than physics.”

This change is being driven in part by demand. Fusion is increasingly being positioned as a potential source of continuous, carbon-free energy for energy-intensive users such as data centers. But ambition alone will not determine the outcome. The companies that will succeed will be those that can build, finance and operate energy systems that meet utility expectations for cost and reliability.

Mowry’s bet is that fusion can ultimately scale more like manufacturing than megaproject infrastructure, enabled by standardized designs and a more streamlined regulatory path than traditional nuclear. Type One’s model reflects this view: rely on experienced partners for non-fusion systems, integrate into existing network infrastructure, and focus internal efforts on core technology.